TL;DR: If you invoice after delivery and don’t charge interest, you’re already offering 0% financing — probably for weeks or months. Big brands turn this into a sales weapon. You should too. Reframe your payment terms as a benefit, use it in your marketing, and protect yourself with clear policies. What was once invisible becomes irresistible.

ATTN: Entrepreneurs

You might be offering one of the most powerful incentives in business — and you’re not even talking about it.

Worse, you’re probably giving it away for free.

I’m talking about 0% financing — the kind of language that moves product off shelves, closes deals faster, and boosts conversion rates across industries. It’s a proven sales magnet, and yet most solopreneurs and small business owners fail to use it.

Here’s the kicker: if you’re delivering work before you get paid, you’re already providing it.

Let’s unpack why that matters, how you can weaponize it in your marketing, and how to do it without putting yourself at risk.

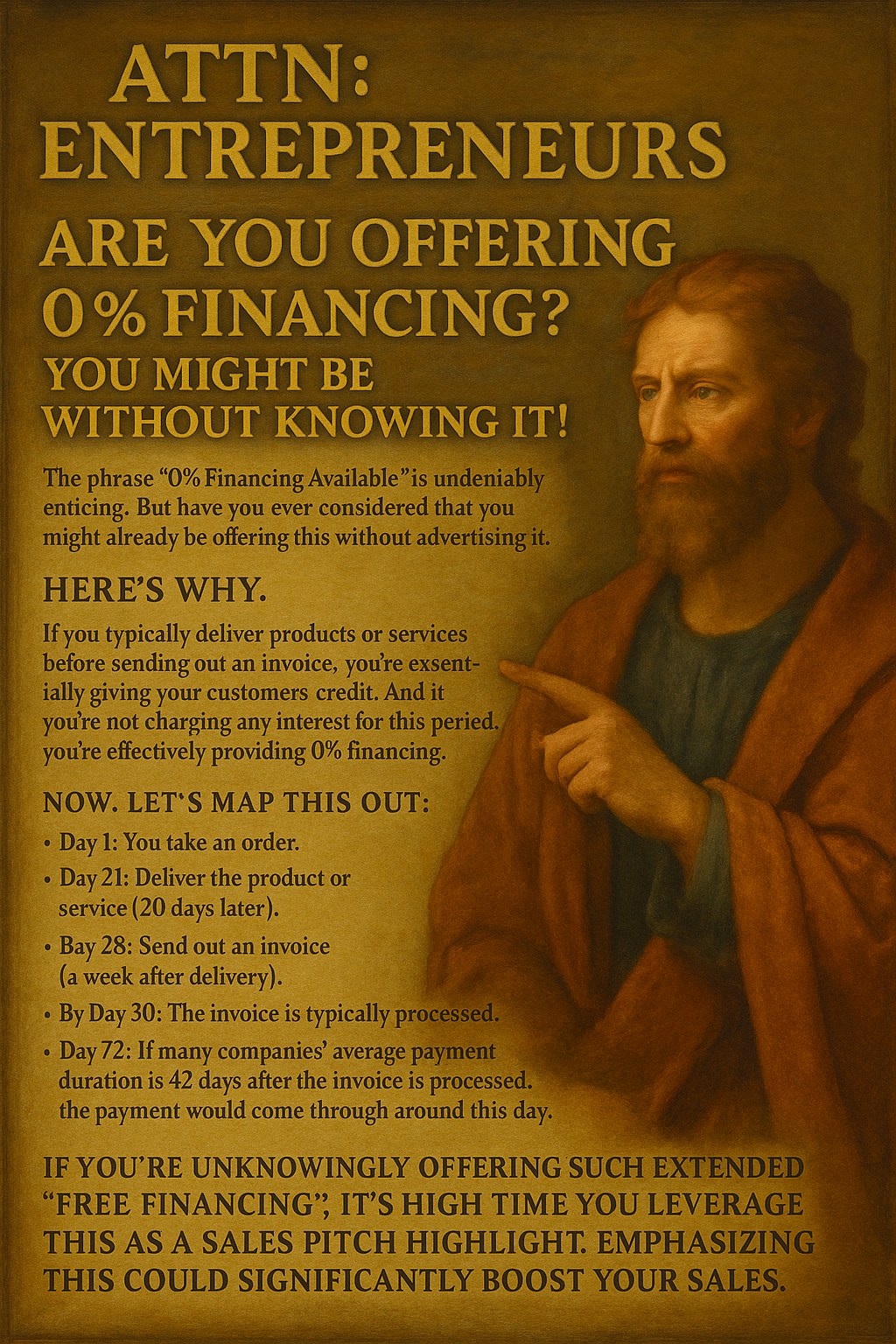

The Financing Offer You’re Already Making

Most small businesses follow a simple pattern without thinking much about it:

- Day 1: A client books your service or orders a product.

- Day 21: You deliver the work (three weeks later).

- Day 28: You send an invoice (a week after delivery).

- Day 30: The invoice is received and enters their payment system.

- Day 72: You get paid (about six weeks later, on average).

From the client’s perspective, they didn’t part with a dime until 72 days — over 10 weeks — after committing to the purchase.

From your perspective, you financed that deal — interest-free — for more than two months.

If you’re not charging late fees, interest, or penalties, you’ve essentially given them a zero-percent loan to buy from you. And most of the time, you’re not even telling them about it.

That’s a missed opportunity. Because what looks like normal business operations to you is actually a highly attractive sales feature — and the bigger players in your market already know how to exploit that.

Big Brands Milk This Strategy — And You Can Too

Look at how major retailers, service providers, and software companies present their payment terms:

- “Buy now, pay later.”

- “No payments for 90 days.”

- “0% financing available to qualified buyers.”

The terms themselves are rarely groundbreaking. But the framing is everything. They don’t say, “We’ll invoice you in 30 days.” They say, “You can get this today without paying until next quarter.”

It’s the same mechanic — just wrapped in language that highlights customer benefit instead of business process.

The lesson is simple: perception is part of the product. And right now, your customers don’t perceive the credit you’re extending as a benefit — because you haven’t told them it is one.

Why Most Small Businesses Miss This Trick

There are three main reasons small operators and solo founders don’t use this strategy — and none of them are good excuses:

- “That’s just how it works.” You deliver, you invoice, they pay. It’s business as usual. Except “business as usual” is rarely the most profitable way to run a business.

- “It’s not a selling point.” Actually, it is. Access to credit, payment flexibility, and cash flow management are huge decision factors for buyers — especially other small businesses. Positioning yourself as an easy, low-friction option gives you a competitive edge.

- “I don’t want to seem desperate.” Offering terms isn’t a sign of weakness. It’s a sign of trust, confidence, and customer focus. Framed properly, it elevates your perceived professionalism.

The truth is, buyers love flexibility — especially if they don’t have to ask for it. If you’re already offering that flexibility, own it.

The Math: How Much Credit Are You Really Extending?

Let’s put some real numbers on this.

Imagine you sell a $5,000 service. You deliver the work three weeks after the order, invoice a week later, and get paid 42 days after that.

That means you’ve effectively financed $5,000 for 72 days — without charging a cent of interest.

If that client had gone to a bank or used a line of credit, they’d be paying interest on that money. If they put it on a credit card, the interest would be double digits. But with you? It’s free.

You might see that as “just the cost of doing business.” But to your client, it’s an invisible benefit worth real money.

So why let it stay invisible?

Reframing: From “Invoice Terms” to “Financing Options”

This is where the magic happens — when you stop describing what you do from your perspective and start describing it from the customer’s perspective.

Bad:

“We invoice on completion, with net 30 terms.”

Better:

“We offer up to 60 days of 0% financing on all standard projects.”

Bad:

“Payment is due 30 days from invoice date.”

Better:

“Secure our services today and enjoy flexible, interest-free payment terms.”

The first version is admin language. The second is sales language. One gets skimmed over. The other gets remembered.

It’s not about lying or overpromising. You’re not changing what you do — you’re changing how you communicate the value of what you do.

How to Implement This as a Marketing Strategy

Once you reframe your terms as a benefit, you can weave it into your entire marketing and sales process. Here’s how:

1. Add it to your sales materials.

Include a simple line like “Interest-free terms available” in proposals, quotes, landing pages, and sales decks.

2. Make it a feature, not a footnote.

Highlight it near pricing or in comparison tables. “Competitor A: 50% upfront. Us: Start today, pay later.”

3. Qualify it if necessary.

If you’re worried about abuse, phrase it as “available to qualified clients” or “included with standard engagements.” This makes it sound exclusive — and protects you from risk.

4. Create options around it.

Offer a small discount for upfront payment or extended 0% terms. This not only gives clients choice but also lets you influence cash flow strategically.

5. Train yourself to mention it.

When speaking to prospects, say things like, “Most of our clients appreciate that we offer 30-60 days of interest-free payment terms — it makes cash flow easier.”

Optional: Turn It Into a Premium Perk

Want to go a step further? Make extended terms a feature of your premium package.

For example:

- Standard clients: 30-day terms

- Premium clients: Up to 90 days interest-free

This turns something you were giving away for free into a lever you can use to increase revenue per client. It also makes the premium tier more appealing without adding much extra cost.

Protect Yourself: Boundaries and Risk Management

Of course, there’s a reason many small business owners don’t talk about this: payment risk is real. Late payments can cripple cash flow, and some clients will exploit generous terms if you’re not careful.

Here’s how to stay safe while still leveraging this strategy:

- Put terms in writing. Always. Verbal agreements are invitations for abuse.

- Use invoicing software. Automate reminders and track payment timelines.

- Set clear boundaries. After a certain point (say 45 days overdue), switch from “interest-free” to “interest-accruing.”

- Know your client. Offer flexible terms to trusted partners and new clients after a vetting period.

- Don’t be afraid to enforce. Respectful but firm follow-ups protect both your business and your reputation.

Remember: this isn’t about being a bank. It’s about marketing the credit you’re already giving — while staying in control of the terms.

What This Really Signals to Clients

There’s a deeper psychological effect at play here too. When you present your payment terms as a benefit, you’re signalling a few powerful things:

- Trust: You’re confident enough in your client to extend terms.

- Stability: You’re financially solid enough not to need immediate payment.

- Professionalism: You understand their cash flow reality and are willing to accommodate it.

These signals build credibility — and credibility closes deals.

Case Study: The Consultant Who Closed 40% More Deals

A solo marketing consultant I worked with recently took this exact advice. She’d been delivering projects and invoicing net 30 like everyone else. Nothing unusual.

But she started framing it differently. Instead of sending proposals with “Payment due 30 days after invoice,” she added a section titled “Flexible Payment Options” that said:

“All standard projects include up to 45 days of 0% financing to help you manage cash flow without slowing down growth.”

That single change bumped her close rate by nearly 40%.

She didn’t offer a discount. She didn’t lower her price. She didn’t change her payment policy.

She simply marketed the invisible value she was already providing.

The Bottom Line: Stop Giving Away Free Money Quietly

Here’s the hard truth: if you’re delivering before you’re paid, you’re already financing your customers. You’re already giving them free money. And if you’re not telling them, you’re leaving a powerful marketing lever untouched.

This isn’t about manipulating clients or playing games. It’s about positioning — taking a cost you already carry and turning it into a feature that helps you sell more, faster, and at higher margins.

In a world where big companies sell “Buy Now, Pay Later” as a premium perk, you can’t afford to keep hiding the fact that you’re doing the same thing — often for longer and with more trust involved.

So don’t bury it in the fine print. Put it in your pitch. Put it in your proposals. Put it in your pricing page. And watch how a single phrase — 0% financing available — changes how clients see you.

Because you’re already offering it. Now it’s time to get credit for it.

StayFrosty!

~ James

Q&A Summary:

Q: What is the blog post suggesting small businesses do with their 0% financing?

A: The blog suggests small businesses should reframe their payment terms as a benefit in their marketing strategy. Instead of viewing it as a normal business operation, they should highlight it as a sales feature like big brands do, offering flexibility and easy, low-friction options to customers.

Q: What is the common payment process for most small businesses?

A: Typically, a client books a service or orders a product (Day 1), the work is delivered three weeks later (Day 21), an invoice is sent a week after delivery (Day 28), the invoice is received and enters the client's payment system (Day 30), and the payment is received about six weeks later (Day 72).

Q: Why should small businesses highlight 0% financing in their marketing strategy?

A: Highlighting 0% financing in marketing makes it a powerful incentive for customers. Access to credit, payment flexibility, and cash flow management are huge decision factors for buyers. Framing it as a benefit rather than a business process can give businesses a competitive edge.

Q: How can small businesses implement 0% financing as a marketing strategy?

A: Businesses can add it to their sales materials, make it a feature rather than a footnote, qualify it if necessary, create options around it, and train themselves to mention it. They can also turn it into a premium perk for certain clients.

Q: What are some ways to manage risks associated with offering 0% financing?

A: To manage risks, businesses should put terms in writing, use invoicing software, set clear boundaries for when interest begins to accrue, know their client well, and not be afraid to enforce payment terms. This helps them to stay in control of the terms.